If you’re looking at to get, then contact the borrowed funds officials within Tidewater Home loan Features, Inc

November 9, 2024Puesto que Badoo inscribiri? creo para acontecer un lugar donde puedas

November 9, 2024Money Their Modular Domestic when you look at the 8 Methods

This article title loans in NJ is section of the Definitive Help guide to Strengthening Standard. This task-by-step article have a tendency to assist you through looking for, choosing, and you will making an application for a standard home loan to assist fund your new home.

When funding modular residential property, banks will usually point your that loan you to experiences a few degree. These are labeled as design-to-permanent loans. Until your home is done and you may get the final appraisal, the loan would be a homes loan. During this period, you create interest only payments. Given that home is over, the mortgage can be a permanent home loan. At that time, you can easily start making regular money contrary to the overall loan amount.

Step one Rating a great Prequalification Guess

Pick should be to score an excellent ballpark figure having how much cash you can easily devote to the new home. For individuals who offer your own financial with economic guidance and you can a general credit rating, they shall be capable offer you a quotation on how much cash they might getting ready to give you and exactly what the interest pricing and you will charges would appear to be. This guess is entirely low-joining, for you and the lender.

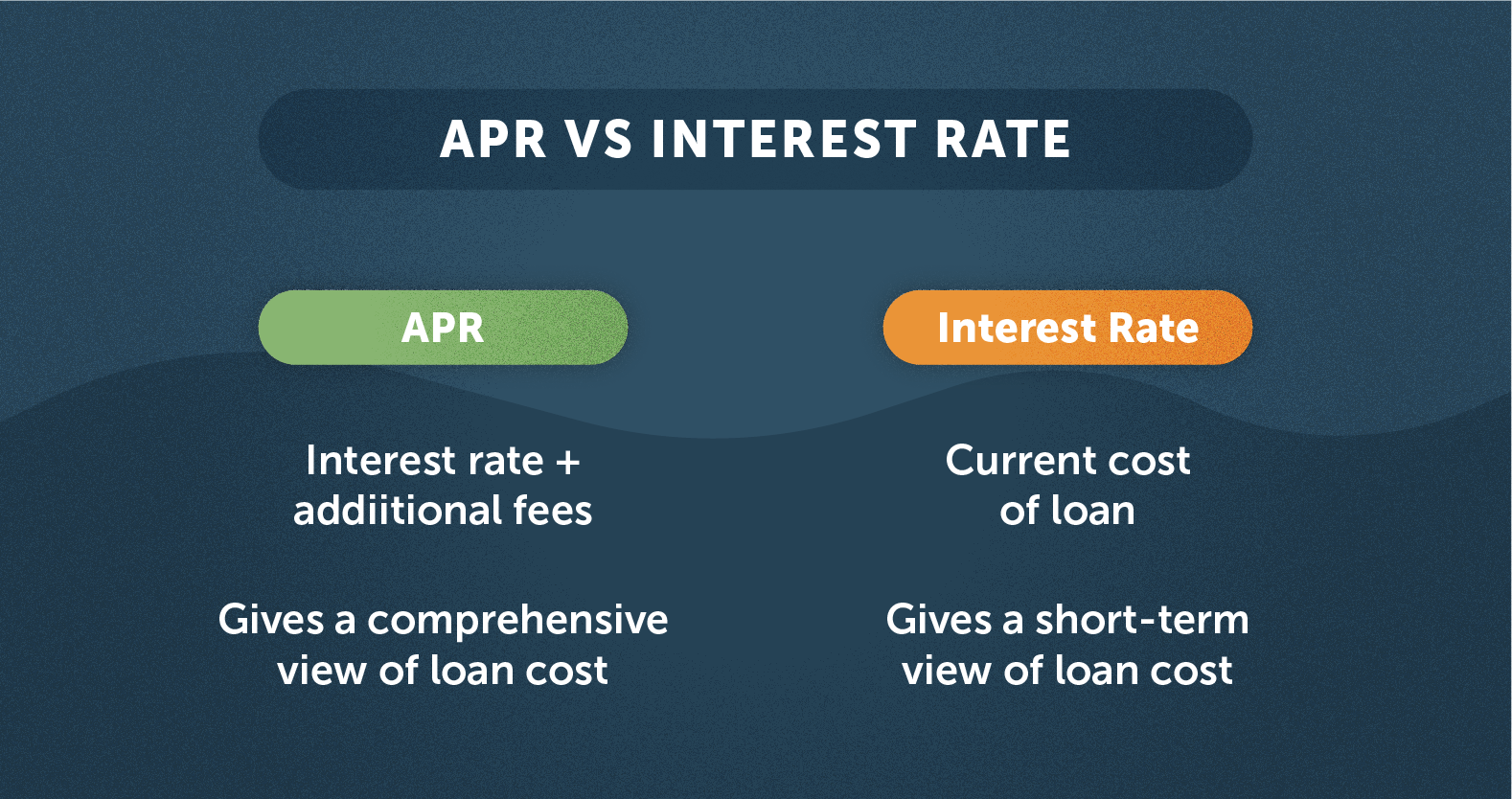

2 Contrast Rates

Rating estimates away from at least step three other financial institutions to see just what version of pricing you can get. Even a positive change from an excellent hundredth out of a portion area distinction within the a performance can indicate several thousand dollars along side lives of loan.

3 Apply

As soon as your believe is done and you picked out land to make towards the, you will must get the borrowed funds. So you can pertain you will need:

- This new price towards the brand name with the home you plan to help you pick

- Your own W-2s on the previous a couple of years

- Irs Function 4506-T

- Government Tax returns (1040s)

- Reveal account of your property and debts

- Proof employment

- Functions Records over the past 5 years

- Your own most recent pay stubs, or if notice-working, proof money out of an excellent CPA

- Information on any the loans

Step Get approved

In case the application is satisfactory, the financial institution tend to agree the loan of the sending you a page from partnership. You may need to tell you it letter to your company otherwise so you’re able to a vendor if you’re to get house in advance of might signal a final price. Note that in the 3 we asserted that you might need your own package attain accepted. It gifts you with some a capture-twenty-two. None the lending company neither the maker desires to be the basic you to definitely assume people chance, you could get them to provide unofficial approvals in order to satisfy the fresh concern of the almost every other team.

Action 5 Arranged a great Disbursement Schedule

Once you discovered finally approval, you will have to expose a timeline to have buying the home, the manufacturer, the overall specialist, and every other costs associated with design your home. Since the each milestone was achieved, the lending company will need proof of achievement, will using an examination. This may make sure only if a task is done to the latest bank’s pleasure tend to fee become create.

Action 6 Romantic toward Mortgage

Since the fresh disbursement agenda might have been set and you can arranged and any other concerns they had did you discover the building enable? was addressed, the borrowed funds could be finalized. You and the financial institution commonly indication the past records therefore will pay closing costs.

Step eight Create your House

During the time that the house is getting created, you’re going to be and make notice costs toward bank monthly. Up to you reside done, you will never be able to make any payments from the idea, so you should ensure you get your family done as quickly as it is possible to.

Action 8 Help make your Structure Loan a long-term Home loan

Shortly after build could have been complete, the bank have a tendency to always check and appraise our home. In the event the everything is sufficient, the mortgage will end up a long-term financial and you can initiate and come up with money against both notice and dominating. Regardless of if up until now you’d a housing loan, this new clock become ticking on the home loan whenever the financing closed. For individuals who got out a 30 12 months mortgage and it grabbed you 3 months to-do build, you’ve got 30 many years and you will nine days kept to invest from the balance. This may mean that their average percentage is a bit high four weeks so you can account for the low number of fee days.