Megabucks Slot Modern Jackpot 10,008,567 Wager Real money inside the Vegas Gambling enterprises

October 18, 2024Best 7s to Burn mobile Payment Gambling enterprises in australia 2024

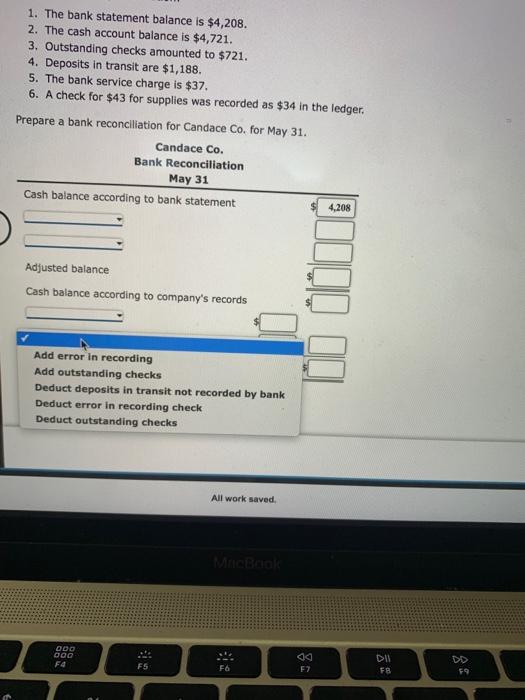

October 18, 2024Thereupon currency fastened, it’s more difficult in order to question this new money

CDFIs establish an alternate exposure character and tend to be rated in another way off a cards angle centered on FHFA recommendations, Donovan said inside the a job interview.

Which month, the brand new FHFA is expected to discharge a research explaining regulatory and legislative proposals which could most readily useful align your house-mortgage banks’ things making use of their congressional mandate in order to offer economical houses financing. In an announcement, this new institution said it is finalizing advice and an easy way to increase help to own lenders doing one particular to possess neighborhood advancement and you will homes.

Changes concerned is a cover to your fund that FHLBs build so you can higher loan providers, Bloomberg Reports said in the Summer. Officials are also considering ways to provide even more financial firms, including nonbank mortgage brokers, the capacity to borrow away from FHLBs to bolster the latest system’s union so you can mortgage brokers, some body always the condition told you history month.

There are lots of notice in our discussions using them into the sensible property and you can people financing, Winthrop Watson, President of your own Pittsburgh FHLB, told you of discussions that have authorities during the a job interview which have Bloomberg history month. We can carry out on you to top that could really incorporate rather to your team.

Varying conditions

FHLBs have fun with unique tax holidays and you will bodies support to improve financing inexpensively in bond segments. They then transfer lowest rates towards the financial serious link institutions, borrowing unions and you will insurance firms that comprise the bulk of the membership.

Larger finance companies are given even more flexibility because of the FHLBs getting credit currency as they are thought to be so much more economically voice. In place of rigid equity conditions, they’re able to usually rating a larger lien on the courses. CDFIs usually face highest borrowing from the bank costs and frequently make other styles from funds to aid the organizations that cannot become bound to use on FHLBs, based on interview with well over several including lenders, newest and you will previous bodies authorities and staff of one’s program. The difference during the treatment is so stark one occasionally higher personal financial institutions render society loan providers greatest entry to investment than simply the brand new FHLBs themselves.

Bodies want banks to pay and provide attributes for reasonable- and you may reasonable-earnings People in the us, plus one of the ways they’re able to fulfill such criteria try by giving credit to help you CDFIs. But in place of the government-paid FHLBs, the big finance companies usually aren’t able to supply the lower costs and choices for much time-identity funds, that are you’ll need for financial credit.

Automobile financing, loans or any other assets aren’t acknowledged

Community loan providers are often the only way so you can homeownership for all of us particularly Tara Carmichael, an enthusiastic ultrasound technical during the Newark, Ohio, which told you she is actually for a long time incapable of score financing that have conventional financial institutions inside her city. Mom out of four went to TrueCore Government Borrowing from the bank Relationship, and that advised their particular tips talk about an effective 580 credit rating. The following year, Carmichael’s score is actually 685 and you will she had a home loan that have TrueCore to find their particular earliest house.

It informed me and this playing cards to blow off, which ones to reduce upwards, told you Carmichael, 43. It hunt much more happy to provide those with lower credit a great options.

TrueCore gets to 70% of its mortgage loans to lower-money consumers. Of a lot investors commonly willing to get such financing, deeming them too high-risk, therefore the team have to keep the personal debt for the their books.

The financial institution keeps a great $43 billion line of credit in the Government Financial Bank regarding Cincinnati but may simply guarantee unmarried-family mortgage loans given that guarantee. Because of this, TrueCore mostly hinges on this new FHLB currency to help you subsidize your house financing it should retain, unlike for new mortgage loans, said Chief executive officer Jason Hall.